It’s not been quite six months since I’ve taken a deep(ish) look at the state of senior housing/senior living. My last post was in December of last year Not much has changed overall in terms of occupancy trends but overall, the industry is faring better than it has since the Pandemic, yet weakness for developers continues. Performance is still challenged by labor costs and overall commodity costs. Real Estate Market and Sr. Living Update – Reg’s Blog

Market Performance and Occupancy

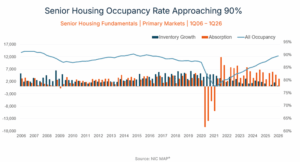

Senior housing fundamentals strengthened in the first quarter. Occupancy rose by 0.4 percentage points, bringing occupied units to another record high. At the same time, year-over-year inventory growth fell to new lows, while annual asking rent growth accelerated for both independent living and assisted living. Senior Housing First Quarter Investment Performance Was Strongest in Nearly a Decade | NIC

- The occupancy rate in the 31 NIC MAP Primary Markets increased 0.4 percentage points to 89.5%, as positive net absorption outpaced the limited number of new units delivered.

- At the current pace, occupancy is on track to exceed 90% before the end of 2026.

- Both independent living and assisted living occupancy rates in the 31 Primary Markets rose 0.4 percentage points during the quarter.

- Independent living surpassed 91% occupancy for the first time since 2016 in both the Primary and Secondary Markets.

- These gains reflect both choice-driven demand from younger or healthier older adults moving into independent living and need-driven demand from residents seeking assisted living services and care.

Supply and Construction Trends

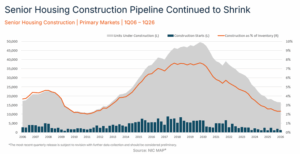

Limited new supply continues to support occupancy growth. Inventory expansion has slowed significantly, and the development pipeline remains historically weak despite improving demand conditions.

- In the 31 NIC MAP Primary Markets, the slowdown in new supply has helped push occupancy higher.

- Year-over-year inventory growth fell to record lows: 0.4% for assisted living and 0.3% for independent living.

- Development activity remains subdued even as occupancy improves.

- Total units under construction fell to roughly 16,400 in the first quarter, a level last seen in 2012.

- Construction underway now represents only 2.3% of existing senior housing inventory, among the lowest levels in the historical series.

- This shrinking pipeline suggests that new supply is unlikely to accelerate meaningfully in the near term.

Pricing and Move-In Discounts

In 4Q 2025, discounts between asking rates and initial rates widened in independent living, increased slightly in assisted living, and narrowed in memory care.

- Independent living (IL): Discounts averaged 12.1% (a3581) in December 2025, equivalent to a 1.5-month discount on an annualized basis, up from 0.9 months in September 2025.

- Assisted living (AL): Initial rates averaged 8.0% (a3556) below asking rates in December 2025, equal to a 1.0-month annualized discount, up slightly from 0.9 months in September 2025.

- Memory care (MC): Discounts averaged 8.2% (a3750) in December 2025, or a 1.0-month annualized discount, down from 1.3 months in September 2025.

Impact of the Residential Housing Market

The residential real estate market has had a mixed but important effect on senior housing demand. In many cases, it has delayed resident transitions, even as demographic tailwinds and limited senior housing supply have continued to support strong occupancy growth.

Many seniors—particularly those moving into independent living, assisted living, or continuing care retirement communities—depend on the sale of their primary residence to unlock equity, pay entrance fees, or cover ongoing costs. While high home prices can support these moves, slow sales, low inventory, elevated mortgage rates, and the so-called lock-in effect often delay transitions.

Long-Term Demand and Supply Imbalance

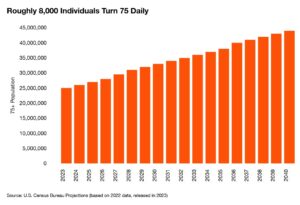

Despite these residential headwinds, senior housing demand has rebounded strongly. Demographic momentum—especially as Baby Boomers begin turning 80 in 2026—combined with unusually constrained new supply has helped push occupancy and rents higher.

- Demand is outpacing supply as record-low unit deliveries and favorable demographics fill communities faster than new properties can be built.

- Rents have increased by roughly 4% year over year, reaching record highs.

- Longer-term estimates suggest the market will need approximately 549,000 additional units by 2028 and 806,000 by 2030, representing an investment gap of roughly a3275 billion under current utilization assumptions.

- At today’s pace, new deliveries are meeting only about one-third of projected demand.

Construction remains constrained by the same pressures affecting other property types, including higher financing and building costs. As a result, the number of new units breaking ground has fallen below the number of units being delivered online—a pattern last seen in 2021 and, before that, during the Global Financial Crisis in 2009.

In several markets, more units are being taken offline than delivered, resulting in flat or negative inventory growth. In addition, more than half of the 140 metro areas tracked by NIC MAP currently have no active development projects.

Senior housing is experiencing a period of constrained supply due to factors impacting all property types, including increasing financing and construction costs. As a result, the number of new units breaking ground has fallen below the number of new units arriving online, a trend that last occurred in 2021 and, before that, in 2009 during the Global Financial Crisis.

Further, in several markets, the number of units being taken offline outnumbers the number of new units being delivered, resulting in flat or even negative inventory growth. Finally, over half of the 140 metro areas tracked by NIC MAP lack a single development project.

Bankruptcy and Operator Stress

Operating challenges remain in various markets across the industry. Despite improving occupancy, too often it comes with incentives that erode margin. Operating cost pressures remain in terms of credit costs and restrictions, rising labor costs, and rising commodity and supply costs. For some operators, passing along costs increases is not in amounts adequate to stave off bankruptcy.

- 13 Chapter 11 filings in senior living/care (independent living, assisted living, CCRCs, skilled nursing) — an 18% increase from 11 in 2024.

- This made senior care one of the only healthcare subsectors (along with hospitals) to see rising filings while total healthcare bankruptcies fell ~21%.

- From 2019–2025: 83 filings total, with over half involving $10M–$50M in liabilities. 2025 ranked among the more active years (behind only 2019 and 2023 at 15 each).

- Senior care accounted for a significant share (~24%) of all healthcare bankruptcies since 2019.

Senior housing and care bankruptcies remain elevated relative to the broader healthcare sector, although most cases are concentrated among small- to mid-sized operators and often involve restructuring rather than liquidation. Post-pandemic cost pressures continue to drive filings even as stronger operators benefit from improving occupancy, rent growth, and net operating income.

Key bankruptcy trends:

- In 2025, the sector recorded 13 Chapter 11 filings across independent living, assisted living, CCRCs, and skilled nursing—up 18% from 11 filings in 2024.

- Senior care was one of the few healthcare subsectors, alongside hospitals, to see rising bankruptcies while total healthcare filings declined by roughly 21%.

- From 2019 through 2025, the sector saw 83 filings in total, with more than half involving liabilities between a310 million and a350 million. By volume, 2025 ranked among the more active years, behind only 2019 and 2023.

- Senior care has accounted for roughly 24% of all healthcare bankruptcies since 2019.

- The sector continued to lead, or tie for the lead, in bankruptcy volume in Q1 2026, with four filings, as overall healthcare Chapter 11 cases rose 33% versus Q4 2025.

- CCRCs with large entrance-fee refund obligations have been especially vulnerable, with at least 15 to 16 filings since around 2020 and significant effects on resident deposits.

Ongoing pressures include:

- Labor and staffing costs, inflation, interest rates, and reimbursement challenges, particularly in care-intensive segments dependent on Medicaid or Medicare.

- An uneven recovery in which weaker or overleveraged operators continue to struggle with lease-up, occupancy gains, and debt service, while well-capitalized owners and operators report strong NOI growth.

- A concentration of distress among smaller, middle-market operators, with fewer but more visible cases among large platforms.

Even so, the broader senior housing market remains resilient. Occupancy is approaching 90%, new supply is limited, rents are rising, and investor interest in acquisitions and distressed assets remains active. In many cases, bankruptcies result in asset sales or operator transitions rather than closures, with resident care prioritized throughout the restructuring process.